The global marine insurance market is doing well. Premium volume in 2023 stood at 38.9 billion USD, up 8.7% on 2022, the highest growth rate in the last ten years.

This trend is underpinned by the intensification of trade on a global scale, the increase in the value of insured vessels, and the consolidation of the offshore sector, which is benefiting from a stable environment.

The world fleet

By the end of August 2024, 18% of the world fleet was owned by China. Greece and Japan come second and third, with 16% and 11% respectively.

Read also | Marine insurance: liability and risks covered

Evolution of the marine insurance market

Over the past five years, from 2019 to 2023, the marine insurance market has seen a 35.54% growth in underwriting. Over this period, premium volume had risen from 28.7 billion USD in 2019 to 38.9 billion USD in 2023. This upturn came after a period of “soft” markets that had lasted until 2015, and a period of fluctuation between 2016 and 2018.

Despite this turnover improvement, marine insurers remain vigilant. Certain threats are still looming and could change the situation namely:

- ever-increasing hull repair costs,

- the occurrence of major fires, aggravated by the risk of transporting electric vehicles and their batteries,

- geopolitical tensions in certain zones and marine routes.

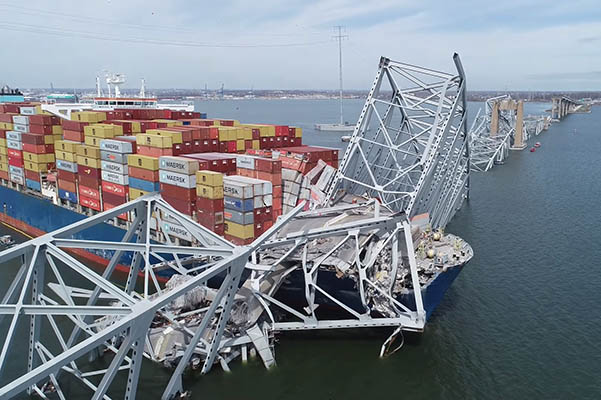

The “Safety and Shipping Review 2024” report, published by Allianz Commercial, highlights the high risk associated with war and climate change. It is worth remembering that 2024 saw a major loss, one of the biggest ever recorded by the marine class of business, namely that of the container ship “Dali”, which destroyed a section of the Baltimore Bridge worth almost 1.2 billion USD.

Breakdown of marine insurance premiums by region

Overall, the breakdown of marine insurance premiums by region has remained more or less unchanged.

In 2023, European insurers accounted for 48.5% of premiums, followed by operators in Asia-Pacific (28.1%), Latin America (10.9%) and North America (7%). The other regions of the world accounted for just 5.5% of premiums.

Over 10 years, the European market has declined by 4.1 points, while the Asia-Pacific market grew by 3.1 points.

Over five years, that is, between 2019 and 2023, Europe has timidly regained ground. Meanwhile, China has made great strides, with its percentage of global marine cargo premiums rising from 11.3% to 14.4%.

Breakdown of marine insurance premiums in 2023

| Region | 2023 shares |

| Europe | 48.5% |

| Asia/Pacific | 28.1% |

| Latin America | 10.9% |

| North America | 7% |

| Other regions | 5.50% |

| Total | 100% |

Evolution of marine insurance premiums by type of coverage

In 2023, the marine cargo coverage was the main transport cover underwritten, with a 56.8% market share, followed by marine hull insurance (23.6%), offshore energy (11.9%) and marine liability (excluding P&I) at 7.7%.

All these lines of business have seen an increase in premium volume compared with 2022, with +7.8% for marine cargo insurance, +10.8% for marine hull insurance, +9.5% for offshore energy insurance and +7.1% for liability insurance.

Figures in billions USD

| Coverage | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2022-2023 evolution |

| Marine cargo insurance | 16.9 | 15.8 | 14.9 | 16.4 | 16.6 | 16.5 | 17.2 | 18.9 | 20.5 | 22.1 | 7.80% |

| Marine hull insurance | 7.6 | 7.5 | 7.1 | 6.9 | 7 | 6.9 | 7.1 | 7.8 | 8.3 | 9.2 | 10.80% |

| Offshore/energy | 5.9 | 4.5 | 3.6 | 3.4 | 3.4 | 3.3 | 3.6 | 3.9 | 4.2 | 4.6 | 9.50% |

| Third party liability | 2.2 | 2.1 | 1.9 | 2 | 1.9 | 2 | 2.1 | 2.4 | 2.8 | 3 | 7.10% |

| Total | 32.6 | 29.9 | 27.5 | 28.7 | 28.9 | 28.7 | 30 | 33 | 35.8 | 38.9 | 8.70% |

Maritime transport: lower loss experience by 2023

Progress in marine safety is now undeniable. In the 1990s, the market recorded an average of over 200 total losses of ships over 100 gigatons per year.

Allianz's annual report on marine shows that total ship losses have fallen sharply, with an average of 73 ships totally lost over the last ten years.

In 2023, only 26 vessels over 100 tons were completely unusable (lost, sunk or grounded), that is, a reduction of 37% compared with 2022, and 71% compared with the average over the last ten years. With 2 951 claims in 2023, the total number of incidents also fell by 2.8% compared with 2022.

This improvement is accounted for by a number of factors, including the tightening of safety standards and the improvement in the general condition of the fleets.

Total losses of vessels over 100 GTs: 2014 - 2023

| Year | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

| Number of vessels | 89 | 105 | 102 | 95 | 74 | 71 | 66 | 60 | 41 | 26 |

The IUMI report confirms this downward trend in losses. In 2023, the number of reported marine cargo incidents with a value in excess of 250 000 USD fell by 25.7% to 535 accidents. The cost of marine cargo claims also follows the same trend, falling by 54.1% to 590 million USD in 2023, compared with 1285 million USD in 2022.

Maritime transport: loss experience by region

The concentration of marine traffic in the South China, Indochina, Indonesia and Philippines region increases the risk of accidents. This region alone has reported 8 total ship losses in 2023, or 30.7% of worldwide losses.

The second highest risk region is the Eastern Mediterranean and Black Sea, with 6 losses.

Other geographical and meteorological factors, such as the frequency of storms, passage through difficult navigation zones, or seismic activity in certain regions, increase the risk of ship loss. .