With 96.348 billion USD in non-life premiums written in 2023, California is the largest insurance market in the United States.

As in other states, standard homeowners' insurance in California typically covers wildfire-related losses.

Unfortunately, home insurance rates, which are regulated by State authorities, are largely too low to cover the high claims, particularly those caused by extreme weather events like the devastating fires of 2017 and 2018, which put significant strain on insurers.

These insurance companies which are not entirely free to set their rates, are also penalized by the high value of new homes built in vulnerable areas highly exposed to forest fires.

Read also | California wildfires

Insurers' reluctance in California

In addition to inadequate rates, California homeowners' insurers face worsening conditions due to climate change, which further increases wildfire claims and inflation.

Faced with this challenging situation, many U.S. insurance companies, such as Allstate and State Farm, began refusing to underwrite new homeowners' policies in California or renew existing ones as early as 2019.

Timeline of U.S. companies withdrawing from the California market:

- 2022, Insurance giant AllState stopped underwriting new homeowners' policies,

- 2023, AmGUARD ceased underwriting homeowners' insurance policies,

- 2023, Falls Lake informed the California Department of Insurance of its intention to completely withdraw from the State,

- May 2023, State Farm and AIG suspended new property insurance underwriting for businesses and individuals,

- Early 2024, Hartford Financial Services Group suspended new homeowners' insurance underwriting,

- March 2024, State Farm canceled 72 000 homeowners' policies. In July, the same insurer canceled approximately 1 600 insurance policies in Pacific Palisades, the richest neighborhood in Los Angeles. Over 2 000 other insurance policies in two other Los Angeles neighborhoods were also canceled,

- May 2024, American National Insurance stopped underwriting homeowners' insurance,

- July 2024, Tokio Marine America Insurance and Trans Pacific exited the California market.

In total, seven of the twelve largest insurance companies active in the California market have suspended or restricted the issuance of new policies in the State.

At least four other insurers have completely left the state (Falls Lake, Tokio Marine America Insurance, Trans Pacific, and Farmers Direct Property and Casualty Insurance Company).

As a result of this withdrawal policy, 10.5% of property owners, or approximately 806 600 Californians, are left without insurance coverage.

Réaction des autorités d’assurance californiennes

To prevent the worsening of the uninsured situation, California's regulatory authorities have adopted a series of preventive measures, including:

- Protecting policyholders for one year against non-renewal or cancellation of homeowners' insurance policies in disaster-stricken areas,

- Limiting geographical exclusions,

- Encouraging insurance companies to return to California,

- Incorporating reinsurance costs into homeowners' insurance rates,

- Encouraging insurers to develop and market coverage proportional to their market share across the entire state of California,

- Using satellite imagery and artificial intelligence (AI) tools to better cover and pool wildfire risk and prevent insurer withdrawals from the market,

- iEncouraging insurers to use risk modeling tools to determine rates.

Read also | Wildfires: a threat to insurers

California's State insurance plan

To address the limitations and restrictions of the private insurance market, California established a public coverage system in the 1960s called the "FAIR Plan." This plan has seen its acceptance capacity increase year after year, with 450 billion USD in current capacity, compared to 50 billion USD in 2018.

However, the FAIR Plan offers only one type of policy, "dwelling-fire," with limited coverage. Moreover, this coverage is more expensive than standard products from private insurers.

The compensation limits offered by the FAIR Plan are 3 million USD for individuals and 20 million USD for businesses, far below those offered by private market players.

California wildfires: the cost for reinsurers

The main players in the reinsurance market will inevitably be impacted by the January 2025 California wildfires.

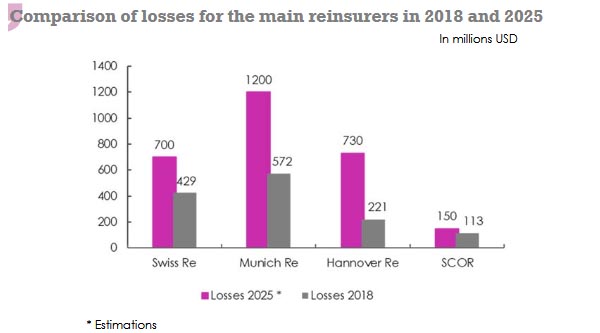

According to Munich Re, this disaster is considered to be the largest wildfire loss ever recorded by the industry, with the German reinsurer being impacted to the tune of 1.2 billion USD by this loss, estimated at between 35 and 40 billion USD.

To protect against potential losses from such events, Munich Re has reduced its commitments and portfolio in the California region.

Other players in the reinsurance market will also be impacted by the latest California disaster:

- Berkshire Hathaway will incur losses estimated at 1.3 billion USD,

- Swiss Re, faced with losses estimated at over 700 million USD, is expected to see its results for the first quarter of 2025 significantly affected,

- Hannover Re is facing claims worth 730 million USD,

- RenaissanceRe, based in Bermuda, will be impacted to the tune of 750 million USD,

- SCOR estimates its net retrocession loss at approximately 150 million USD, before tax.