The Covid-19 health crisis, which changed policyholder behavior and led to the widespread use of teleworking, accelerated the transformation of motor insurance that had been in the making for a decade.

The quickly recovered technical equilibrium following the pandemic prompted insurers to invest massively in new technologies. Global insurance leaders such as Ping An (China), Allianz (Germany), AXA (France), Zurich (Switzerland), All State and Geico (USA), supported by reinsurers Munich Re, Swiss Re and Hannover Re, are playing a key role in the development of motor insurance.

Their contribution can be seen in a number of strategic and operational areas, from innovation and regulation to risk management and improving the customer experience.

Motor insurance: Customized insurance plans

Teleworking, introduced on a large scale during and after Covid, has led to fewer commutes, prompting insurers to review and expand their offerings.

Usage-based motor insurance has picked up. This model, which already adjusted premiums according to mileage or driver behavior, is booming, as policyholders want premiums to reflect their actual use of the vehicle. Such adjustments allow safe drivers to benefit from rate advantages. This model is becoming increasingly popular, especially with the success of connected cars.

Since then, innovative solutions have continued to emerge. The use of Big Data and telematics to monitor driving habits via in-vehicle devices or mobile applications gives insurers greater flexibility in adjusting premiums to the risks and needs of their customers.

Motor insurance and the rise of electric cars

According to the International Energy Agency (IEA), recourse to electric vehicles is well underway, despite tariff barriers, rising customs duties and the introduction of protectionist measures against Chinese manufacturers. The IEA estimates that more than 20% of vehicles sold worldwide in 2024 will be electric, a rate poised to climb to 48% in 2030.

The global fleet of electric vehicles in circulation is currently estimated at 45 million, half of which are in China. To date, 31 countries, including 18 in the European Union, have adopted this type of vehicle.

The future of the electric car depends on innovation by manufacturers, improved vehicle performance (especially in terms of range), pricing and tax incentives.

A concern for insurers, however, is that the claims experience of electric vehicles could prove high. In the event of an impact, the lightweight aluminum bodywork would require the intervention of specialized bodywork specialists. What's more, battery-related repairs could represent up to 50% of the vehicle's cost.

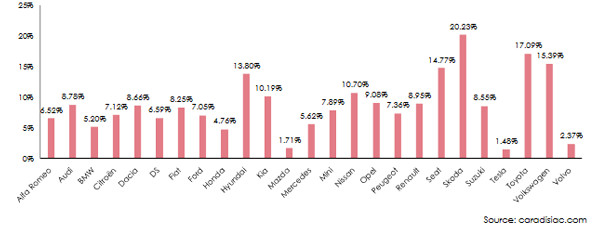

Rising vehicle value

With the rise of fully electric and hybrid cars, and the introduction of new technologies and on-board systems, the value of new vehicles continues to rise.

In just one year, brands such as Skoda, Toyota and Volkswagen have seen the value of their vehicles rise by over 15%.

Motor insurance and the development of autonomous and connected vehicles

The emergence of autonomous and connected cars is bringing about a major transformation in the motor insurance sector.

According to research firm Counterpoint, 50% of new cars sold worldwide today are connected to the internet and equipped with information and communication services.

AI-enabled vehicles offer opportunities to improve operational efficiency, better manage risks and detect anomalies. While they potentially reduce the risk of accidents, they also raise complex issues relating to liability in the event of a claim. In the event of damage caused by a connected car, several parties may be held liable: the vehicle manufacturer, the driver, the subcontractor, the manufacturer of the software equipping the vehicle, the equipment supplier, etc. This is a new technological reality to which insurers must adapt.

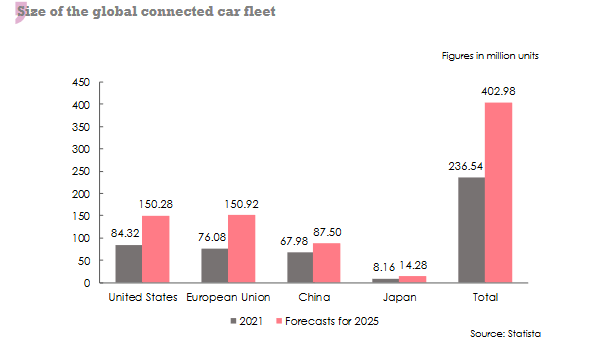

In 2021, the global fleet of connected vehicles stood at 236 million units. It reached 350 million in 2023 and should exceed 400 million in 2025.

According to Autopromotec Observatory, a US firm specializing in the study of connected vehicles, projections for 2027 point to a market of over 640 million such vehicles.

Read also | Challenges facing the motor insurance market

Motor insurance and artificial intelligence integration

The use of mobile applications and digital tools such as Chatbots has become commonplace among motor insurers compelled to manage and underwrite risks. These applications are designed to facilitate underwriting, contract management, claims processing, image-based damage estimation and fraud detection.

Connected objects, telematics devices and smartphones are essential working tools for insurers' business models. They enable real-time access to information (driver behavior), improved customer experience (customized coverage and customized pricing), better understanding of risks and rapid claims management.

Thanks to the use of artificial intelligence, a Ping An policyholder can notify a claim online, upload photos of the damage, receive an automatic assessment of the claim within seconds. For small claims, compensation is then immediately transferred to the policyholder after confirmation by facial recognition.

The use of Blockchain is also considerably contributing to the insurance market, allowing fast, clear management of large data flows, while ensuring the traceability and security of information and transactions linked to a claim.

Rate increases

Since 2022, the general trend has been for motor insurance prices to rise in many countries, with the United States, Canada, the United Arab Emirates and Germany undergoing significant rate increases. In France, the increase in motor rates, which has remained moderate over the past two years (+7% over two years), is likely to rise sharply to 6% in 2025.

Following the sharp rise in rates in 2022 and 2023, the United Kingdom and Saudi Arabia (+50% to 100% for motor Third Party Liability) reported a fall in motor rates in 2024.

Below is a sample of 2023-2024 rate trends in selected markets.

| Country | 2023 | 2024 |

| United States | 11% | 13% |

| Canada | 10% | 7% à14.5% |

| United Arab Emirates | 20% | 20% à 25% |

| Saudi Arabia | 50 à 100% | -25 à -35% |

| Egypt | 30% | ND |

| Germany | 11% à 13% | 18% |

| France | 3% | 4% |

| United Kingdom | 50% | -1.50% |

| India | ND | 13.6 |

NA: Not Available

Source: Atlas Magazine

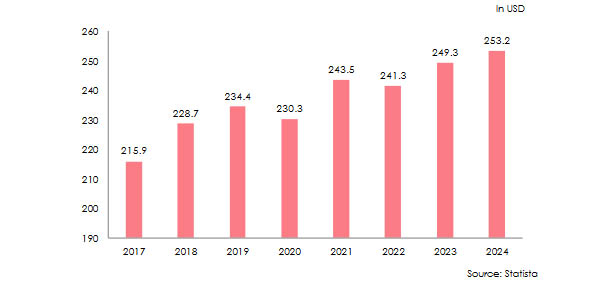

Globally, with the exception of 2020, the year of Covid-19, and 2022, the year of the post-Covid economic slowdown, the average premium written per capita (total global premiums divided by global population) has been growing steadily.

This average premium has risen from 215.9 USD in 2017 to 253.2 USD in 2024, an increase of 17% over seven years.