Takaful insurance is an insurance concept in line with the Islamic faith, based on solidarity, mutual responsibility and cooperation. The fundamentals of the model are based on the Qur’an, the Sunna (1), and Fiqh (2) which prohibit:

- Riba : usurious interest,

- Gharar : the sale of an uncertain or random product, which forms the basis of a conventional insurance contract,

- Maysir : gambling, speculation.

(1) These are the words, deeds and judgments attributed to the Prophet Mohamed

(2) The temporal interpretation of the Qur’an and Sunna

The principles of takaful insurance

Derived from Islamic law, the financial system of takaful insurance is based on four principles:

- Participant or insured contributions are made in the form of donations (premiums).

- The sums collected are paid into two separate funds:

- the participants’ fund which is designed to pay out claims. The latter must be clearly separated from the shareholders' fund.

Participants' contributions are placed in a mutual investment fund managed in accordance with Shariah principles, where profits and losses are shared between the participants and the takaful operator. Any surplus funds after settlement of claims and management fees are distributed to participants in the form of rebates or dividends. - the shareholders' or management fund, which covers management expenses.

- the participants’ fund which is designed to pay out claims. The latter must be clearly separated from the shareholders' fund.

- Participants, who are also policyholders, receive a redistribution of the technical surplus of the fund dedicated to them. This process transforms them into true partners.

- The establishment of a "Sharia Board" or Sharia oversight council. Made up of leading figures with expertise in Muslim law, this board's mission is to ensure that the company's contracts and management comply with Islamic principles.

Takaful insurance classes of business

As with conventional insurance, takaful business is divided into two main activities:

- Family Takaful which, depending on local legislation, is either equivalent to traditional personal insurance (life + health and individual accident insurance), or only to the life class of business (life and death) of the traditional insurance scheme.

- General Takaful. As with traditional insurance, this heading covers property damage and liability risks underwritten by individuals and companies.

There are also "composite takaful" companies that underwrite products that fall under both Family and General takaful business.

As with direct underwriting, the takaful reinsurance market is also divided into Family Retakaful, General Retakaful and Composite Retakaful.

Takaful insurance: management methods

Takaful insurers do not all adopt the same operating model. There is no universal standard for managing a company. Each country has its own organizational structure.

There are four main business models, with variations possible for each:

- Mudharaba

- Wakala

- The Hybrid model

- The Waqf model

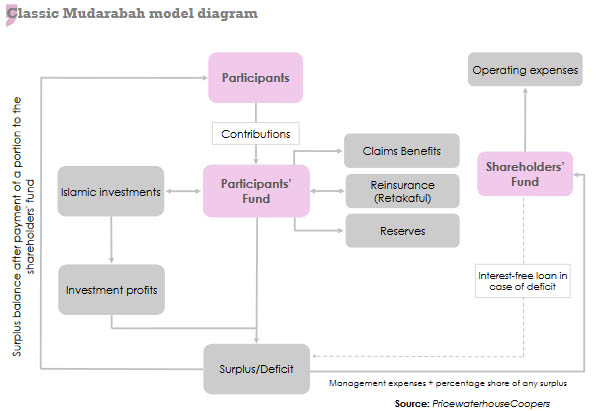

The Mudharaba model

This is a form of financial partnership in which risks and profits are shared between the participants' fund and the shareholders' fund.

The Mudharaba contract sets out how the takaful company's profits are to be shared between the two funds.

However, certain general takaful products (property and casualty insurance), which contain few savings components, make it difficult to adopt this model. Hence the need to make some adjustments to incorporate surplus sharing.

As shown in the diagram below, the surplus or deficit resulting from underwriting operations and investment profits flows into the shareholders' fund and the participants' fund.

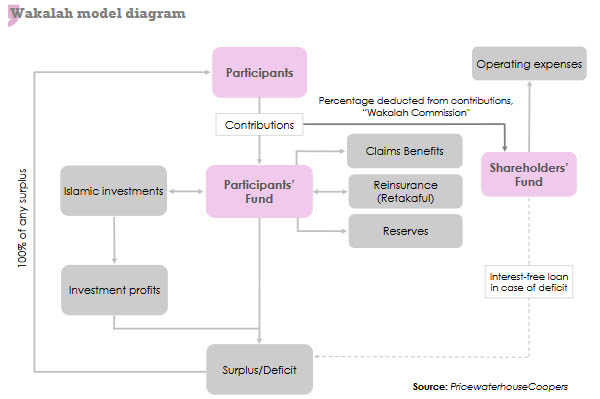

The Wakala model

Wakala, or "representation" in Arabic, is based on contributions. Policyholder contributions are divided, according to a pre-agreed percentage, between two funds: the participant or policyholder fund, and the management or shareholder fund. In this sharing model, there are no profits or losses between the two funds. These profits or losses are charged in full to the participants' fund.

The shareholder fund thus acts as an agent, receiving a fixed commission agreed in advance and subject to the approval of the Sharia board. This model is mainly used in the Middle East.

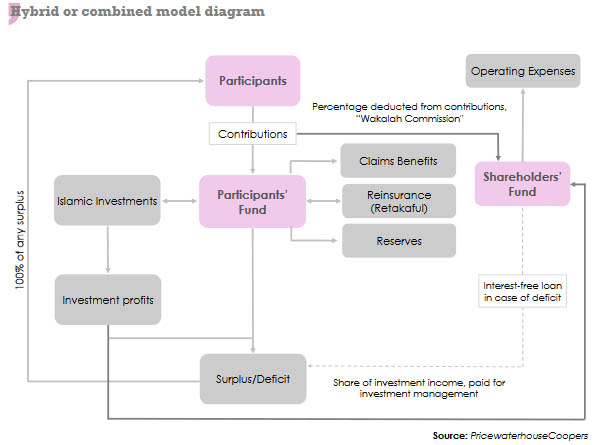

The hybrid or combined model

The hybrid model, recommended by AAOIF I (1) combines certain aspects of the Wakala and Mudharaba models. It capitalizes on the advantages of both approaches.

The shareholder’s or manager’s fund signs two contracts with the participant fund:

- A first wakala-type contract as fund manager, with remuneration in the form of a percentage of contributions (bonuses).

- A second, Mudharaba-type contract as entrepreneur. This contract authorizes them to invest participants' contributions. For this activity, they receive remuneration based on the surplus generated.

(1) Accounting and Auditing Organization for Islamic Financial Institutions, based in Bahrain

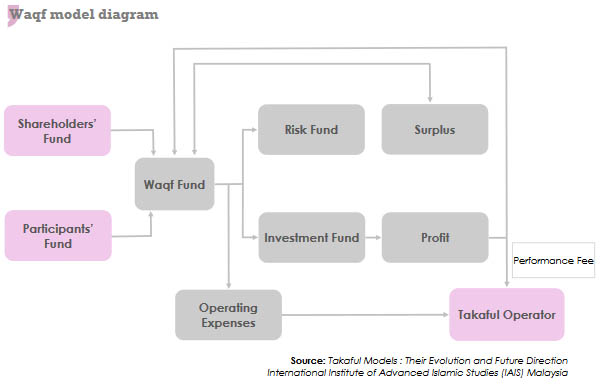

The waqf model

According to Muslim customs and traditions, a waqf is a donation made in perpetuity by an individual to a charitable organization. This donation is inalienable.

Waqf serves two purposes. The first is to provide financial assistance to members of the fund in the event of losses, and the second is to make a donation to charitable organizations.

The waqf operation takes place in two stages:

- In the first stage, the operator (the manager) creates a waqf fund within the takaful fund of which they will be the manager. They will pay an initial contribution and relinquish their ownership rights.

- In the second stage, policyholders pay a portion of their contributions in the form of a donation, in keeping with religious principles of mutual aid.