Bond insurance: definition

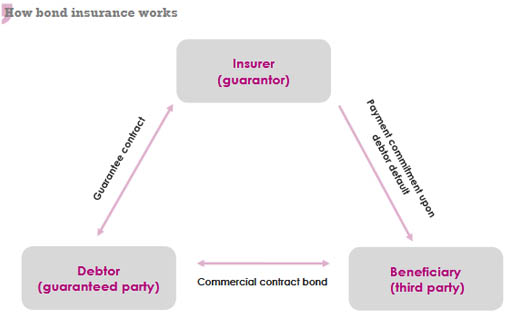

Bond insurance is based on a three-party relationship involving a principal debtor, an insurer, and a beneficiary.

It is a contract whereby an insurer guarantor undertakes to guarantee to a beneficiary (creditor) the fulfillment of a contractual or financial obligation when a company (debtor) fails to meet its obligations.

Accordingly, the insurer acts as a third-party guarantor to protect the beneficiary of the contract in the event of a contractual, financial, or technical default by the service provider.

Read also | Credit insurance and bond insurance

Benefits of bond insurance

Bond insurance features several advantages. It enables companies to:

- enhance their credibility and competitiveness by reassuring clients and partners of the debtor’s ability to honor its contractual obligations,

- optimize their cash flow management by deferring certain payments or anticipating cash inflows. The company does not need to tie up cash, which allows it to have additional resources available for investment or to address unforeseen events,

- preserve their borrowing capacity to finance strategic projects or to protect against economic fluctuations,

- comply with legal and contractual requirements, particularly in regulated sectors such as construction and public works, transportation, or public procurement,

- facilitate access to public procurement markets by providing the guarantee required by government agencies,

- secure commercial relationships as the insurer comes into play to compensate the beneficiary in the event of the company’s default.

Bond insurance: how it works

Bond insurance has been designed to guarantee the proper fulfillment of commitment, covering risks related to the non-performance of work, failure to pay, or non-compliance with regulations, whether in public or private contracts.

This type of guarantee is useful in many areas: construction projects, public works, service provision, license availability, commercial transactions, and compliance with legal requirements.

Bond insurance is underwritten by the debtor (the company that must perform the work or fulfill a commitment) to preserve its cash flow and reassure its partners.

The insurer assesses the risk, analyzes the debtor’s creditworthiness, and determines the terms of coverage, ultimately issuing a surety bond to the beneficiary.

In the event of the debtor’s default, the beneficiary may claim the bond by establishing non-compliance with the obligation. The insurer then compensates the beneficiary and claims reimbursement of the amount paid by the debtor, in other words, the defaulting company. The insurer is entitled to legal recourse against the debtor to recover the sums paid.

The bond, therefore, plays out as a temporary financial guarantee, comparable to a credit commitment, and not as a permanent transfer of risk.

Read also | The different types of surety bonds

Role of the insurer

As a key player in the bond business, the insurer plays a decisive role in supporting businesses by mitigating risks and providing financial security for transactions. To this effect, it draws on its technical expertise, its mastery of the legal framework, and its financial analysis capabilities.

The insurer steps in upon inception of the setup phase to the arrangement: it intakes the debtor’s application, conducts a thorough analysis of the debtor’s financial situation and ability to meet its obligations. Based on this assessment, it sets out the terms of the guarantee and formalizes its commitment by issuing a surety bond for the benefit of the beneficiary.

In the event of the debtor’s default, the insurer compensates the beneficiary in accordance with the agreed terms, and then, if necessary, lodges recourse to recover the amounts paid.

The contrat

The bond agreement binds the three parties to a performance obligation: the debtor (company), the beneficiary (customer/government), and the insurer.

The contract also specifies the maximum guaranteed amount, the duration of the bond, and the conditions under which it may become payable. Finally, it includes clauses regarding the insurer’s right of recourse, while complying with applicable legal and regulatory requirements.

The surety bond

A surety bond is sometimes required to carry out a specific activity, complete a project, or conduct a transaction. It is designed to protect the project’s principal from certain breaches by the contractor and enables the principal to recover the costs incurred.

Generally, and depending on the country, this plan limits can range from 10% to 30% of the contract’s value.

In Europe, Latin America, and Asia, rates range from 10% to 30% of the bond amount, whereas in the United States, they can climb to 100% of the bond value.

The premium

The surety bond premium is generally calculated as a percentage of the total bond amount. According to Swift Bonds, it generally represents a rate between 0.1% and 10% of the bond amount.

This rate varies significantly depending on the country, the market, the type of bond required, the nature of the risk, the industry, the duration of the bond, the amount guaranteed, and the company’s creditworthiness.

For clients with a stable financial profile, the premium is often in the lower range, between 0.1% and 3%. However, it can reach 15% for companies with a very high-risk level.

This is often a one-time premium for fixed-term guarantees, or annual premiums for open-ended contracts.